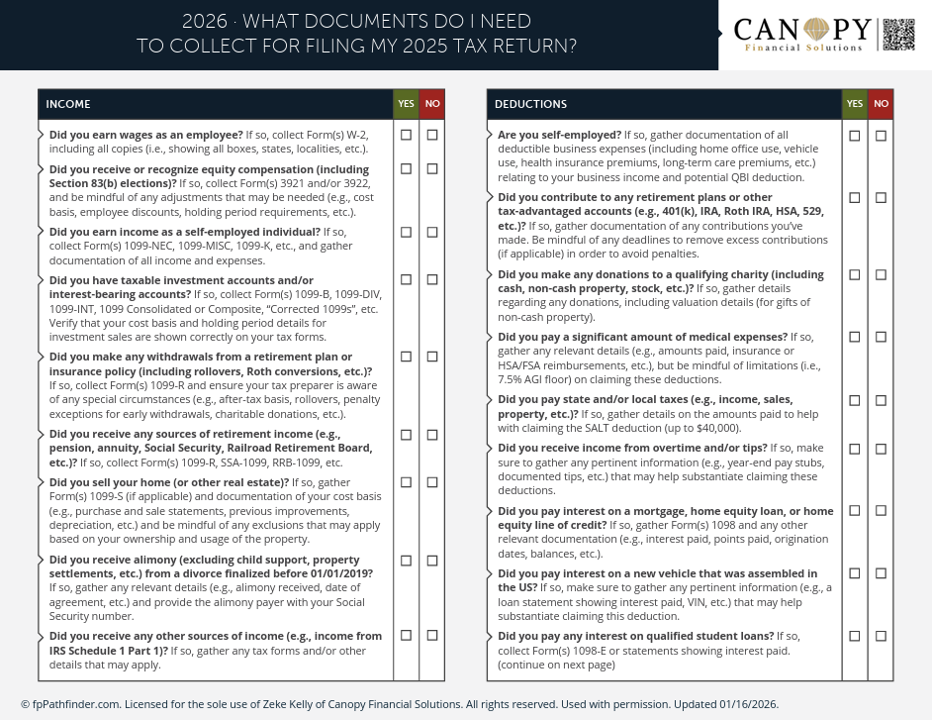

Click Checklist To View and Download

February, 2026: Tax Preparation Tips

Tax season may not be anyone’s favorite time of year, but a little preparation goes a long way toward reducing stress and helping you keep more of what you've earned. As you gather documents and get ready to file, here are a few simple steps to make the process smoother and more organized this year.

1. Get Your Documents Organized Early

Start a dedicated folder—digital or physical—to collect everything you’ll need. Common items include:

W‑2s and 1099s

1098 mortgage interest statements

Realized gains/losses reports

Retirement contribution records

Charitable giving receipts

Health insurance or HSA forms

The earlier these are gathered, the easier filing becomes.

2. Maximize Your Retirement Contributions

You still have time to make 2025 IRA or Roth IRA contributions up until the tax filing deadline. If you're eligible, these contributions can reduce your taxable income or help you maximize tax‑free growth. If you’re self‑employed, double‑check deadlines for SEP IRAs and Solo 401(k)s.

3. Look for Deductions and Credits You May Have Missed

Tax breaks often get overlooked. Make sure to review:

HSA contributions

Child Tax Credit or Dependent Care Credit

Education credits (American Opportunity or Lifetime Learning)

Energy‑efficient home improvement credits

A few minutes of review can lead to meaningful savings.

4. Review Your Withholding and Estimated Payments

If you received a refund that was larger than expected—or ended up owing more than you’d like—it's a good time to adjust your withholding for the year ahead. Small tweaks can help create a more predictable tax outcome.

5. Keep Records of Major Life Changes

Events like marriage, divorce, a new child, selling property, or launching a business can all affect your tax situation. Make sure your records reflect these changes and update your tax professional if anything new happened in 2025.

6. Don’t Rush Your Return

Filing early is smart—but filing accurately is smarter. Wait for all your tax forms before submitting your return (amended returns can be time‑consuming). If something seems missing, request a corrected form from the issuer.

7. Ask for Help When You Need It

Taxes can be complex, especially with multiple income sources, investments, or retirement accounts. You don’t have to navigate it alone—reach out if you’d like help reviewing your financial picture before filing..

-

Click below to view and download these useful guides and resources:

2026 Important Numbers

-

Several new tax breaks are now available for the 2025 tax year (filed in 2026), thanks to recent federal tax law changes. Here are the highlights your family should know:

• New Senior Deduction

Adults age 65+ may now claim an additional deduction of $6,000, or $12,000 for married couples if both spouses qualify.

[kerneldata...covery.com]• New Tip Income Deduction

Workers in eligible tipped occupations may deduct up to $25,000 of qualified tip income, subject to income limits.

[support.mi...rosoft.com]• New Overtime Pay Deduction

You may now deduct the overtime portion of your pay (anything above your regular rate), up to $12,500 for single filers or $25,000 for joint filers.

[support.mi...rosoft.com]• Car Loan Interest Deduction

If you purchased a new U.S.-assembled vehicle, you may deduct up to $10,000 of interest on the auto loan.

[thewindowsclub.com]• Expanded SALT Deduction

The cap for state and local tax deductions has temporarily increased to $40,000 for married couples filing jointly.

[kerneldata...covery.com]These new deductions can meaningfully lower your taxable income and reduce your overall tax bill. If you’re unsure which apply to your situation, I’m here to help you review your documents and make sure you’re taking advantage of every opportunity available.

Additional Considerations and Resources