Weekly Market Updates | 03/16/2026

Market Summary and Performance, ending Friday March 13th, 2026

Capital markets remained volatile for another week as geopolitical turmoil in the Middle East and rising oil prices continued to pressure global sentiment, yet U.S. equities remained relatively resilient with somewhat measured declines. Energy stocks again led the S&P 500, while semiconductors provided key support amid strong earnings takeaways. International markets were mostly lower, with Europe weighed down by stagflation concerns and Asia dented by rising oil prices and credit market jitters. Meanwhile, bond markets saw yields rise and curves flatten as investors pushed out rate‑cut expectations, and crude oil moved higher amid supply disruptions.

Commodities: Oil is the primary market driver. Brent Crude is trading near $100 per barrel, and WTI Crude finished the week around $99.30. In contrast, Spot Silver crashed 4.4% today to $81.34, pressured by a strengthening US Dollar.

Crypto: Bitcoin (BTC-USD) has shown relative stability, hovering around $71,000. While down from its 2025 peak of $126,000, analysts view the current consolidation as a potential accumulation phase ahead of upcoming Fed decisions.

Forex: The US Dollar remains dominant as a safe-haven asset. The EUR/USD pair has crashed to seven-month lows, while the British Pound (GBP/USD) is under pressure near 1.3250.

Key Events to Watch This Week

Federal Reserve Meeting: A critical FOMC decision is expected this week. Markets are currently pricing in a "pause," with persistent inflation from energy shocks reducing the likelihood of 2026 rate cuts.

Nvidia AI Conference: Nvidia (NASDAQ:NVDA) will hold its GTC conference in California. While typically a major catalyst for tech, its impact may be overshadowed by geopolitical developments and oil prices.

Geopolitical Risk: Any further escalation in the Middle East or additional disruptions to shipping in the Strait of Hormuz will likely maintain upward pressure on oil and downward pressure on risk assets.

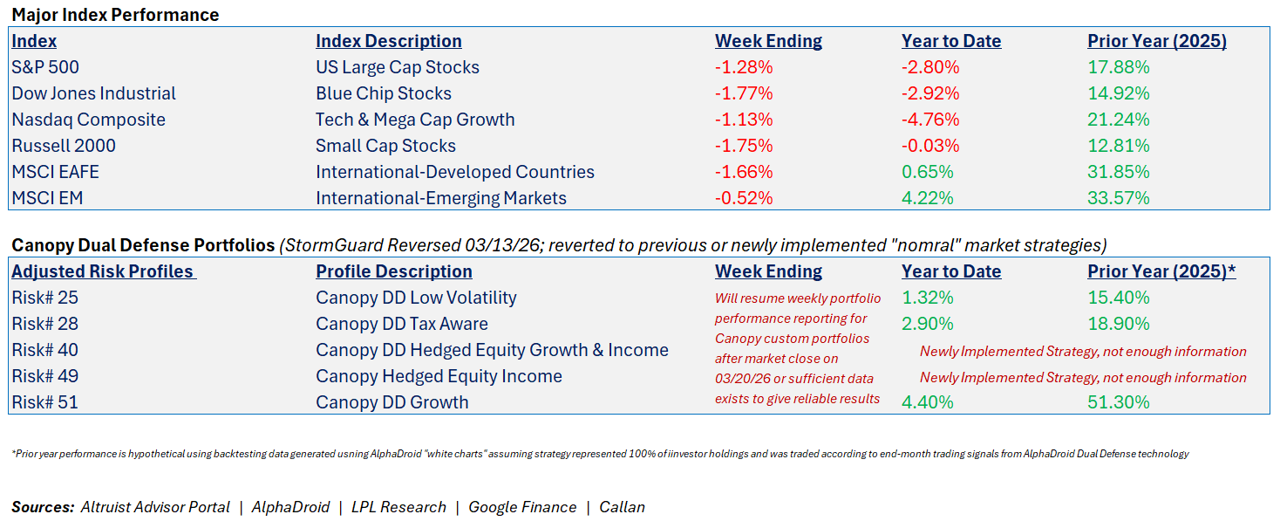

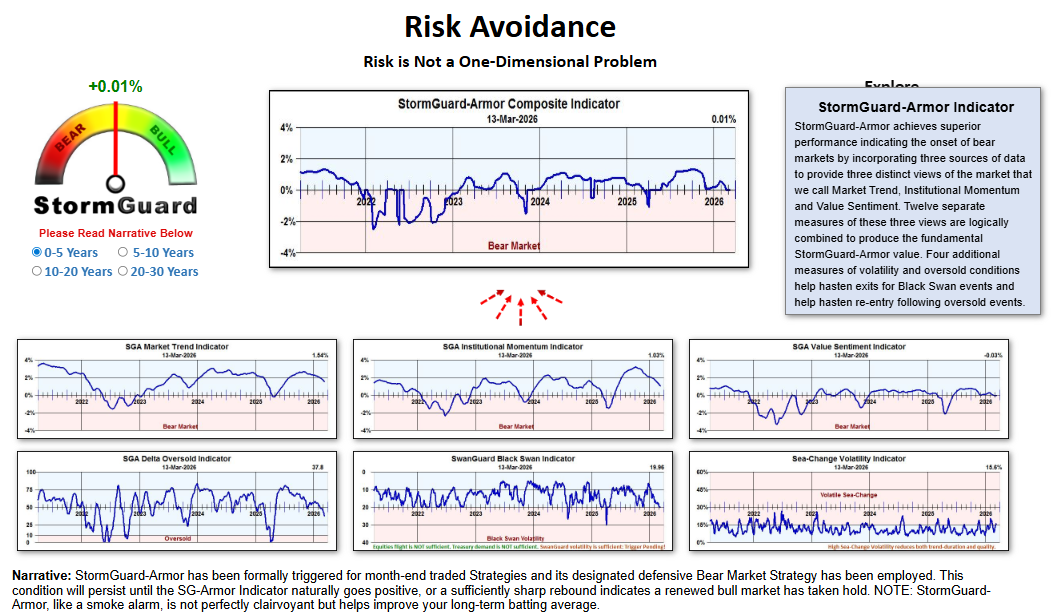

StormGuard-Armor returned to positive territory on 03/13/26 after ending the month negative on 02/27/26, officially triggering month-end trading into defensive Bear Market Strategies for all Canopy Dual Defense Portfolios.

We do not attempt to time the markets or make short-term trading decisions based on random volatility or a “few bad days.”

The StormGuard Composite Indicator is derived from its three primary indicators (also above) plus more than a dozen relatively minor confirmation indicators used to validate the conclusions. The Market Trend Indicator still indicates overall bullish large-cap behavior, as does the Institutional Momentum Indicator. However, the Value Sentiment Indicator (new highs/lows weighted) has been weak and is what influenced the overall negative trigger. This trigger was not likely caused by the new Iran war, the tariffs, the deficit, or the national debt, but it has a character rather similar to the government shutdown last fall.

Very few defensive safe-havens during this recent bout of volatility and Global uncertainty.

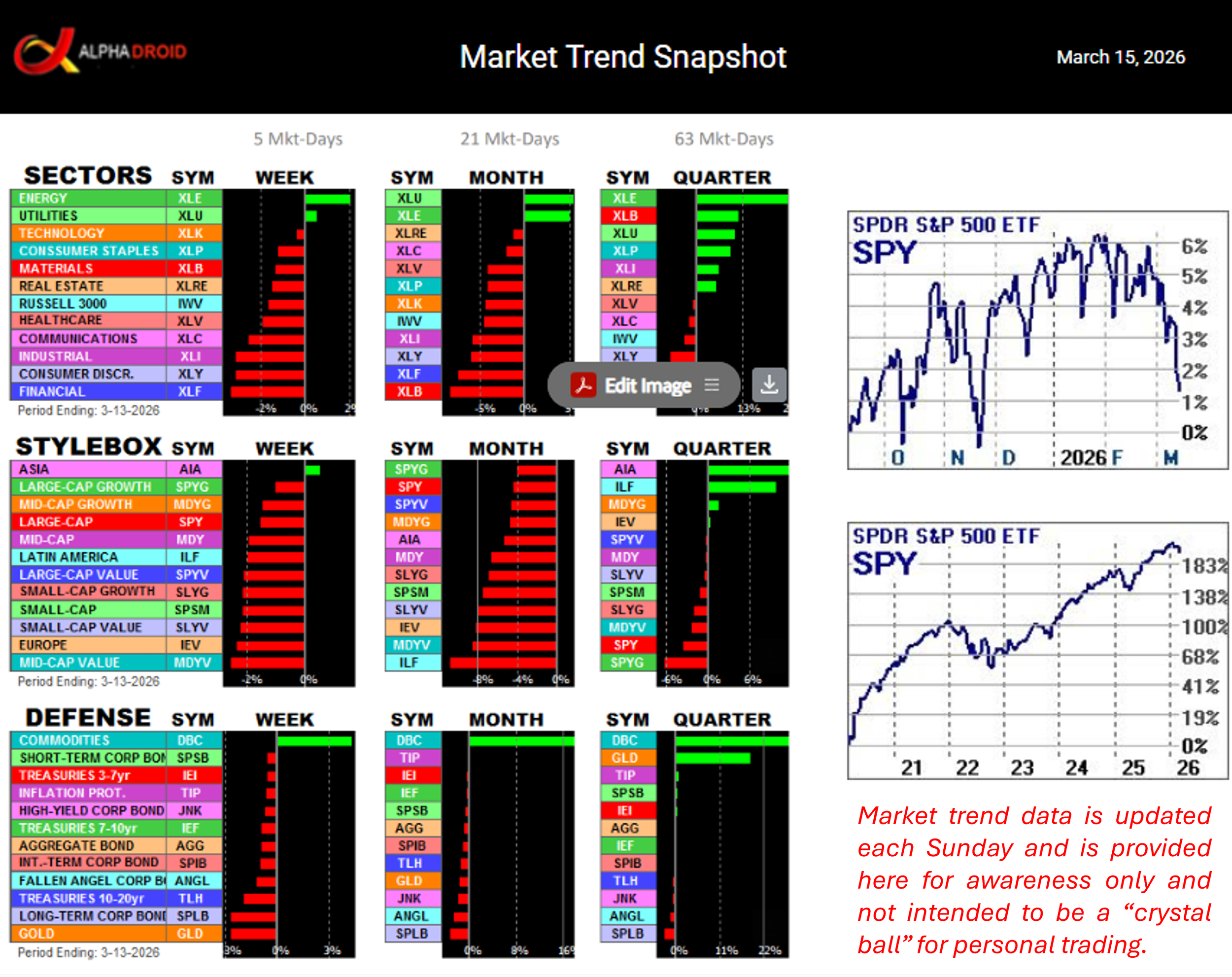

Traditionally, assets like bonds and US Treasuries provide an inverse relationship to the direction of stocks — meaning that transitioning to these assets during market downturns is a great defensive strategy, but as you see in this Market Trend Snapshot, there were very few bright spots in Sectors, Style or Defense for the past 21 days.

For example, while the S&P 500 (along with other indexes around the world) tumbled in 2008, these “Bear Market Strategies” would have returned our clients a very lucrative positive gain, considering we would have followed these same StormGuard indicators and trade signals.

We find ourselves in a unique situation where sitting on the sidelines in conservative bond strategies is not providing the protection we seek. This is primarily because the interest rate environment is so uncertain — while most believed we would continue to see the Federal Reserve CUT interest rates in 2026, lingering inflation concerns may pause those cuts and even necessitate short-term rate INCREASES.

So What — we will return to “normal” market strategies, given the neutral StormGuard rating; however, our portfolio exposure to equities will remain very specific rather than broad index exposure. Additionally, Canopy Dual Defense custom portfolios have been updated and refined to better match individual client risk profiles.